close

Choose Your Site

Global

Social Media

Views: 20 Author: Site Editor Publish Time: 2018-11-16 Origin: Site

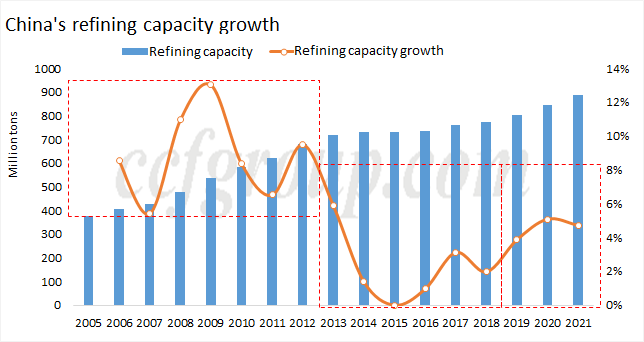

China's refining and chemical industry continues to grow, and its refining capacity has nearly doubled over the past decade. With the implementation of the 13th Five-Year Plan of the petrochemical industry, China's refining capacity will continue to grow in the next few years, but the refinery development route and market structure will change.

China's refining capacity growth

State-owned refineries are dominant among China's oil refining enterprises, with large scale and high operating rate. They are both in the leading positions in crude oil production and refined oil sales. Others are local refineries, which are relatively small in size and mostly concentrated in Shandong Province. In recent years, more private enterprises entered the refining and chemical industry, and several projects are going to be put into production, which is changing the current market structure.

At present, there are a large number of refineries in China, but the scale of a single set is not large, and the regional layout is relatively lack of planning. After the 13th Five-Year Plan, China plans to build seven petrochemical industrial bases, and the newly-built refineries tend to be large-scaled and integrated.

Development of oil product route to chemicals

Traditional refineries mainly focused on refined oil products, including gasoline, kerosene, and diesel. In recent years, new private refineries, especially those that have gradually developed from polyester industry, tend to produce more aromatics and olefins and matching downstream products.

With the continuous upgrading of refined oil, some independent or state-owned refineries are also building new reformers and extracting more aromatics.

Given the above two aspects, the proportion of chemicals in the refining industry is increasing.